How About the Bottom Line First

Navigating the lumber industry’s current landscape isn’t straightforward. Uncertainty over tariffs—whether they will remain, be adjusted, or removed—has left the industry in a holding pattern. This hesitation has stalled movement and slowed operations, creating an environment where even industry leaders are reluctant to make major moves. In addition to tariff concerns, labor shortages, regulatory challenges, and environmental factors are more than mere inconveniences; they’re significant hurdles shaping the market rapidly. Recognizing and openly discussing these interconnected complexities is important for industry stakeholders looking to adapt and succeed in uncertain times.

Lumber prices have been volatile, largely due to industry stagnation caused by policy uncertainty. The influence of evolving policies, international trade dynamics, and internal domestic challenges has further complicated an already strained market. As an exterior trim products manufacturer navigating these challenges firsthand, Belco Forest Products is committed to understanding the broader impacts so we can continue to support our customers while contributing to the long-term integrity of the construction and lumber industries.

A Shifting Foundation: How Policy is Reshaping the Industry

Historically, the U.S. construction industry has always relied on a steady stream of Canadian lumber, which supplies roughly 30% of the U.S. softwood lumber market. An additional proposed 25% tariff, combined with existing duties of 14.5%, totals nearly 40%, significantly straining supply chains. This shift has considerably disrupted the market, leaving many industry professionals baffled and seeking answers.

While these new policy adjustments aim to protect the interests of domestic producers, they have also introduced an immediate volatility that is difficult to navigate, especially for manufacturers, distributors, and builders already facing labor shortages, material delays, and unpredictable costs. Adding another layer of nuance, the executive order to expedite logging in U.S. national forests has sparked renewed debate over environmental impacts, long-term sustainability, and the feasibility of rapidly expanding domestic logging operations.

Filling the Gap: The Reality of U.S. Lumber Supply

As the United States grapples with impending escalating tariffs on Canadian lumber, the feasibility of meeting domestic demand through internal production has come under scrutiny in recent weeks. Rising costs, workforce shortages, and infrastructure constraints are raising concerns about whether domestic production can realistically replace imported lumber. This gives new meaning to the old adage, “You can’t see the forest for the trees.” Many stakeholders find themselves focusing so intently on individual policy decisions or specific disruptions, that they are potentially missing the broader systemic challenges facing domestic lumber production as a whole. The reality is, industry professionals must now endeavor to decode a sophisticated maze of interconnected issues while wading through a significantly disheveled market environment.

Current U.S. Lumber Production Capacity

The U.S. South has emerged as a significant player in the lumber industry, with softwood lumber mill capacity exceeding 28.4 billion board feet in 2024, a 35% increase from 2017. However, ironically, this growth is largely attributed to investments by Canadian lumber companies seeking to capitalize on the region’s abundant timber resources and favorable operating conditions. “Disparity in log costs and availability are the major drivers here, but Canadian investment in the region has certainly been partially motivated to moving operations where they avoid the impact of duties,” said Dustin Jalbert, Senior Economist, FastMarkets. “Even under modest growth scenarios, it’s probably closer to a decade to replace Canadian supply completely (in the U.S),” Jalbert continued, flagging more short-term financial pain for the industry facing multiple challenges.

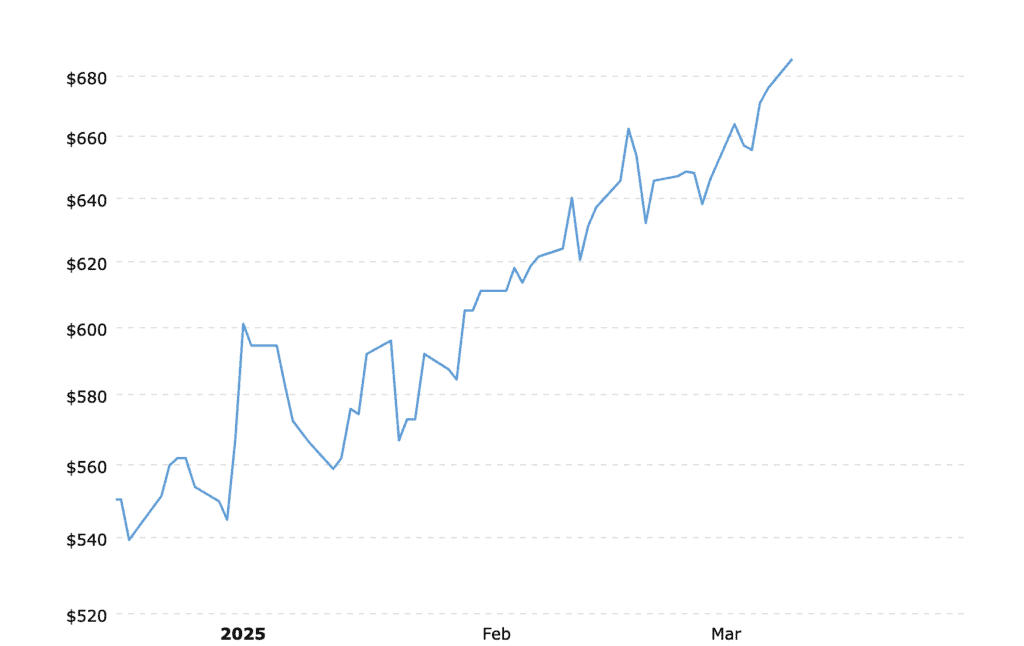

Further complicating matters, the real time price of lumber futures soared past a two and a half year peak. Note the year-to-date lumber price increase just since January from MacroTrends:

George Carillo, CEO of Hispanic Construction Council, has also projected that prices could reach $765 within weeks or months after tariff implementation, pushing the cost increase of a medium sized house over more than $10,000, as reported by Reuters. Compounding these issues, there seems to be no relief ahead from the Fed for interest rates. Consequently, builder confidence is low and has been steadily dropping with each new layer of stifling information since January. This price volatility has left investors apprehensively frozen, deepening market paralysis across the industry.

Labor Shortages in the Logging Industry

A critical factor contributing to underutilization is the labor shortage within the logging sector. The industry has seen reduced employment over the past two decades, with an aging workforce exacerbating the issue. This demographic shift poses significant challenges to scaling up production to meet domestic demand. An aging workforce, with 71% of loggers aged 50 or older, coupled with a lack of younger entrants, poses significant challenges to scaling up production. Les Werner, Former Director of Wisconsin Forestry Center, University of Wisconsin elaborates on this by saying, “It is likely that the general public has a limited understanding of the breadth and magnitude of the resources provided by our nation’s forests, as well as the economic impacts of the industry beyond their local area.

More concerning is the perception, particularly in densely populated areas, that active forest management is not environmentally or ecologically sound. This lack of knowledge and the resulting misinformed perceptions are significant barriers to workforce recruitment.” Additionally, increased mechanization and advanced logging equipment have altered workforce demands, complicating recruitment and training.

Regional Differences in Forest Management

Canada’s Sustainable Approach to Forestry

In Canada, forestry management is guided by a strong emphasis on sustainability and long-term ecosystem health. Canadian provinces enforce rigorous regulations to ensure that harvesting rates do not exceed forest regrowth. This approach is particularly important for the slower-growing species commonly found in Canadian forests. These trees are managed under strict replanting and conservation programs that are intended to help preserve biodiversity and maintain high-quality lumber yields over time.

Such practices are backed by agencies like Natural Resources Canada, which provide detailed guidelines and monitoring systems to balance economic and environmental objectives. These measures are meant to help maintain ecological balance and ensure a stable and responsible supply of lumber.

However, it’s worth noting that many Canadian loggers and mill workers feel the country’s conservation regulations have become overly stringent, viewing them as driven more by political bureaucracy than genuine science-based forestry management. Clearly, responsible forest management has valid perspectives on both sides of the issue. As with most complex, charged topics, genuinely effective solutions are likely to emerge not from heavy-handed policies on either extreme, but from a thoughtful, collaborative middle ground.

The U.S. Diverse and Adaptive Forestry Practices

By contrast, the United States has a more varied approach to forest management, consisting of a patchwork of private, state, and federal lands. This fragmented structure results in a wide range of management strategies, shaped by economic priorities, environmental policies, and landowner objectives.

Fast Growing Southern Yellow Pine

One of the defining characteristics of U.S. forestry is its reliance on fast-growing species such as Southern Yellow Pine (SYP) in the Southeast. This species grows significantly faster than the slow-maturing softwoods found in Canada, allowing for shorter harvest cycles of 25 to 35 years. These rapid growth rates make U.S. lumber production more responsive to market demands, though some foresters caution that shorter cycles may impact wood strength and quality as well as long-term forest resilience.

Pacific Northwest: Douglas Fir and Slower Growth Cycle Species

The Pacific Northwest, in contrast, has shifted its focus in recent decades toward harvesting smaller-diameter trees, as most mills have been optimized for processing smaller logs rather than large old-growth timber. While large logs were once the industry standard, changes in forest management and resource availability have led to an increasing reliance on smaller, more rapidly harvested trees. Species like Douglas fir and Western Hemlock remain prevalent, but the emphasis is now on shorter growth cycles rather than centuries-old timber. The U.S. Forest Service and various state agencies continuously work to balance economic incentives with conservation needs, particularly given the country’s fragmented land ownership and the imperative to manage natural hazards.

U.S. Logging Industry Knowledge Deficit

Perhaps the most pressing factor at play for an expedited expansion of the U.S. logging sector, is the erosion of modern day industry knowledge. Decades of reduced domestic harvesting have led to a significant decline in forestry expertise within the U.S. Forest Service, making immediate large-scale logging expansion a complicated proposition. Many argue that the agency now lacks critical skills in timber management, environmentally responsible harvesting, and market logistics. Rebuilding this knowledge base would require years of training and recruitment. Given these factors, many in the industry believe that relying on federal timber as a primary solution to U.S. supply issues remains highly unrealistic. Unfortunately, stagnant production capacity, labor shortages, and regulatory hurdles are obstacles for the U.S.’s ability to immediately meet its own lumber demand independently.

Environmental and Regulatory Nuances

Beyond the differences in species and harvest cycles, both nations face environmental challenges that influence management strategies. In Canada, preserving old-growth canopies is seen as vital, not only for biodiversity but also as a natural deterrent against wildfires. Similarly, in the U.S., maintaining mature trees is important for fire prevention and habitat conservation. However, the diverse ownership models in the U.S. mean that regulatory frameworks can vary widely. This variability sometimes results in less consistent management practices across regions, complicating efforts to implement broad sustainability measures. While some would consider these inconsistencies a “con” in the overall scheme of things, others argue that logging in the U.S. would be less inhibited by bureaucracy and restrictive environmental policy.

Efforts to boost domestic lumber production by increasing US logging activities will also inevitably encounter regulatory and environmental hurdles. The recent executive order aims to expedite logging in national forests to enhance timber production. However, these initiatives often face industry and public opposition due to environmental concerns, legal challenges, and the complexities inherent in altering federal land use policies. While the intention to bolster domestic lumber production is clear, the reality is riddled with hurdles and linear time delays that leave the market reality of today, floundering.

For stakeholders across the lumber and construction sectors, understanding these nuances is as important as it is overwhelming. Anticipating market trends and informing strategic decisions must balance immediate economic needs with long-term resource stewardship. In this context, both systems offer insight on the interplay between environmental integrity and industry demands.

The Building Code Challenge

While building codes are designed to be inclusive, substantial shifts in lumber sourcing might prompt reevaluation of existing standards. Such revisions are typically deliberate and methodical, involving extensive research and stakeholder consultation. The selection of lumber species in construction directly influences structural integrity, compliance with building codes, and overall project costs. Variations in growth rates and wood characteristics between Canadian and U.S. lumber species present unique challenges and considerations for builders and regulators.

Canadian Lumber: Structural Integrity

Canadian forests predominantly yield slow-growing species like SPF, renowned for their exceptional strength and durability. This species is highly favored in structural applications due to its remarkable dimensional stability and high resistance to environmental forces such as storms and earthquakes. These inherent properties enable Douglas Fir to meet stringent building codes, making it a preferred choice for architects and engineers aiming for robust structural performance.

U.S. Lumber: Variability in Performance

In contrast, the United States extensively utilizes faster-growing species like Southern Yellow Pine (SYP), particularly in the southeastern regions. While SYP exhibits considerable strength, it is more susceptible to warping, expanding, and shrinking compared to Douglas Fir. This propensity for dimensional instability requires careful consideration in construction practices to ensure compliance with building standards. Builders often need to implement additional measures, such as selecting higher grades of lumber or incorporating design adjustments, to mitigate potential issues arising from these characteristics.

Implications for Building Codes and Industry Practices

Building codes in the United States are developed to encompass a wide range of lumber species, including both domestic and imported varieties. The International Building Code (IBC), widely adopted across U.S. jurisdictions, provides standardized guidelines that consider the diverse properties of various lumber species. This comprehensive approach does allow for the use of different types of lumber without requiring immediate modifications to the codes when sourcing shifts between domestic and Canadian supplies. However, any necessary updates to accommodate new lumber species or changes in sourcing practices may create substantial delays, during which builders and regulators must rely on existing guidelines and professional judgment to ensure safety and compliance.

The Future of Lumber in a Shifting Market

With so many factors at play, one fact is undeniable; stabilizing lumber supply and pricing is no simple task. As tariffs on Canadian imports rise and domestic logging policies evolve, the industry must wrestle with issues in every link of the supply chain, from sawmills to construction sites. Expanding domestic production presents its own set of problems that cannot be resolved overnight. Meanwhile, reliance on imports remains complicated by inconsistent trade policies and geopolitical influences.

Key Takeaways:

- Rapidly changing tariff policies and market volatility are actively reshaping lumber supply chains.

- Environmental and regulatory complexities significantly impact industry practices.

- Labor shortages present ongoing challenges to scaling domestic lumber production.

- Thoughtful, nuanced responses rather than blunt-force solutions will better serve long-term industry health.

Recommendations to Consider

- Manufacturers: Diversify supply sources and invest in inventory forecasting tools. Actively explore potential alternative raw materials sources to maintain production stability.

- Dealers and Distributors: Enhance transparent communication with partners, strategically manage inventory, and provide value-added services like just-in-time deliveries, pre-cut lumber packages, or timely market trend reports to support your customer base. Build and/or tighten up relationships with material manufacturers who value on time delivery and supply chain efficiency.

- Builders: Lock in material prices early where possible, adopt flexible project management practices, and maintain clear, proactive communication with clients to manage expectations effectively.

At Belco Forest Products, we recognize that staying ahead in a shifting market requires innovation, adaptability, and a deep understanding of the industry’s complexities. That’s why we remain committed to not only delivering high-quality exterior trim products, but also contributing to the broader conversation, helping our partners navigate uncertainty while advocating for sustainable, forward-thinking solutions. We remain firmly committed to informed adaptability, continuous innovation, and sustainable growth in this evolving industry landscape.